When I started my credit journey in January 2012, all I wanted at the time was the first card, and I stayed with one card for the next 9 months until I learned that there were better cards in the market. For the next 3 months I went on an app spree and finally came to the point where I felt adding another card to my portfolio wouldn’t do me much good any more.

Apparently the number of credit cards I have is absurdly high to many people. The common perception is that more credit cards suggest more financial trouble. Knowing that a high percentage of the population tend to abuse credit and get themselves into a debt spiral, I totally understand how this perception was created.

Needless to say, if you have had credit before and found yourself often charging credit cards up to the maximum allowed and not paying the balance in full, 1 credit card is enough. You still need a credit card to maintain your credit history, but for that purpose one card can be sufficient if you do not abuse it. On the other hand, if you are able to handle credit well, never charge to the limit, and always pay statement balances in full, then you should have multiple credit cards. If you want to know the reason, please read on.

When I had 9 months of credit history to boot and was approved for multiple credit cards, I wanted to be fully aware of the consequences of having many credit cards before I applied for more. Does having more, or fewer, better for your credit history, given that you always pay in full?

Which side would you pick?

My answer: More is better.

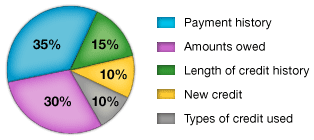

You may recall from my previous posts that your FICO credit score is the most important metric for evaluating your creditworthiness for the next credit application. Ultimately, the purpose of a credit card is to help you build credit. So the use of cards that maximizes your credit score is the best use.

The number of credit cards affects 2 components of your credit score: utilization ratio and average age of accounts.

Utilization ratio is the ratio of the total reported balance to the total credit available. Utilization is directly tied to the amounts owed on your credit cards: obviously when you are wealthier and have more credit available to you, owing a couple of thousand dollars on your credit cards is not a big deal. But if you are fresh out of school without a permanent job and only have $2,000 in available credit, owing $1,500 represents very high risk of default. Having more cards means having more total credit and lower utilization ratio. This will help your score.

Average age of accounts is a measure of “New credit”. It is, well, the average age of all your credit and loan accounts, aka trade lines. The more new credit you have, the lower the average age of accounts. Each time you obtain a new trade line, the average age decreases. The more accounts you already have, the less the decrease in average age will be:

Say you have 9 cards averaging 2 years old, and you obtain a car loan. The new average age will be (2*9+0)/10 = 1.8 years, a reduction of 0.2 years in average age. On the other hand, if you have 1 card which is 2 years old and obtain a car loan, the new average age will be (2*1)/2 = 1 year – your average age of accounts just went down 50%! Your credit score will go down significantly. If you’re going to apply for a mortgage, the reduced average age may cost you tens of thousands of dollars of payments.

So my plan was to concentrate all the cards I wanted to apply for on the earlier stage of my credit building process, so that all the accounts will age together and minimize the damage to credit score from any future trade lines. With 1 year and 5 months of credit history, I am now past that stage, and that’s why I haven’t applied for credit for the last 4 months.

Apart from the credit score, how else does the number of credit cards affect your creditworthiness?

When you apply for credit, sometimes your application is not approved right away. The credit issuer decides that they need a human being manually review your application to determine if they should extend you credit. What would the credit analyst think when he/she reviews your credit profile and sees 20 open credit cards? Either of two things: you have financial trouble, or you are an excellent credit manager.

Why an excellent credit manager? Well, how else could you have handled so many accounts without ever missing a payment? This requires knowledge and discipline. And this is exactly what creditors are looking for in applicants.

Could the number of credit cards be due to financial trouble? Not really, if the most recent card was opened more than a year ago. If you were in debt, you’d have applied for credit last month, or the month before, or the month before. Especially when most of your accounts show a zero balance, and only one or two show positive balances, and small ones at that, the notion that you may be a high risk borrower is unfounded.

To recap my analysis, when you are building credit and not applying for any big loans any time soon, it is better for the long run to have more credit cards. But don’t apply for more credit cards if you cannot handle the current ones, or if you are planning to apply for a loan in the next year or so.

Hope you all have a great weekend!

Best,

Richard (Hiep Tran)

I agree 100% I have a lot too. But the crazy thing is although my aaoa went down my utilazation went way down as I don’t carry to many balances. My scores increased by 30 pointsn in one month! MORE IS BETTER

MYFICO…FICO_addict…

Ps thanks for the advice on ky thread

Way to go! Keep in mind that if you want to maximize your FICO score in preparation for a credit application you should only have one card showing a balance, and keep the overall utilization ratio around 1%.

You’re welcome! Thanks for visiting my blog!

Best,

Richard

hello

how many cards do you have total? and how far apart did you get each? i just got my secured BofA card and wanted to know how you paced yourself so i can have an idea because i also want to apply in my early stages of my credit building so that later there will be less damage to my credit score from new accounts i may open in the future.

-Liz

Hi Liz,

I would recommend pacing the applications 3 or 6 months apart at least. 3 months so that your AAoA recovers, and 6 months so that the impact of inquiries on FICO scores drops. Each time you apply, shoot for 2-3 cards and try to submit the applications at once. That’s what I did and now I’m sitting at 10+ cards with AAoA of 1 year and 1 month and credit history length of 1 year and 11 months. The last card I obtained was obtained in August this year. I am gardening for a high FICO score for my future auto and mortage loans.

If I were you I would wait at least 6 months before applying for your second card to maximize your chance of application success.

hi!

thanks for your reply! i will try that and see how it goes~

will be looking forward to your new posts~ your blog is very helpful 🙂

thankyou,

Liz

Thanks! There will be more good stuff coming soon! Good luck with your financial journey 😉