As a former pension actuary, retirement saving is one of my favorite personal finance topics. I’ve written several posts on 401(k) vs IRA, and today I’ll be talking about the history of these retirement saving plans and making some observations about how the history affects the current retirement saving pictures.

Investing: The mindset

My two-year anniversary with investing is around today. This means I have been owing you this post for 2 years. In the past 2 years, I have spent more time learning about investing and actually investing than doing anything else with my personal finance. And yet I have posted very moderately on investing. The reason is, investing is complicated. Very complicated. I did not feel comfortable sharing my meager knowledge and experience with you in fear of leading you astray in this complex universe. 2 years later, I finally feel that I have something to offer. Continue reading Investing: The mindset

What are the tax advantages of a retirement savings account: Traditional/Roth 401(k)/IRA

Hopefully I have given you enough tease to get you curious about the tax advantages of a retirement savings account. I recommend you peruse these introductory posts to gain a basic understanding of retirement saving before reading this number-heavy post.

Why you should start saving early for retirement

Why retirement saving is not just about saving

Chances are you have heard about the tax advantages of a 401(k) or IRA somewhere before. Let me sum up and illustrate in an easy-to-understand way, and as always, I’m available to answer questions.

Let’s clarify this first: retirement savings accounts have tax advantages over what?

What is an IRA and why you should contribute to it.

Like a 401(k), an IRA is a retirement savings account. You put money in it, and use that money to invest. But unlike a 401(k), an IRA does not have an employment requirement. IRA stands for Individual Retirement Account; anyone, even if he is not employed, can contribute to an IRA unless his income is too high. This works perfectly for freelancers such as my friends that are dancers and do not work for any particular company.

Continue reading What is an IRA and why you should contribute to it.

What is a 401(k) and why you should contribute to it

This post has 3 parts. Part 1, I explain what a 401(k) is. Part 2, I explain how you contribute to a 401(k). Part 3, I explain why you should contribute to a 401(k).

Part 1. What the heck is a 401(k)

A 401(k) is a retirement savings account sponsored by employers. In order to contribute to a 401(k), you need to be employed.

Continue reading What is a 401(k) and why you should contribute to it

Introduction to retirement savings accounts: Traditional/Roth 401(k)/IRA, what are they?

I’m sure you have heard of these terms before. They probably appear on the media more frequently than the Kardashians. Traditional 401(k), Roth 401(k), Traditional IRA, and Roth IRA are 4 types of retirement savings accounts.

The basics of retirement savings: why “saving” may not be enough

“Saving” is a funny word in this context. It may not mean what you think it does.

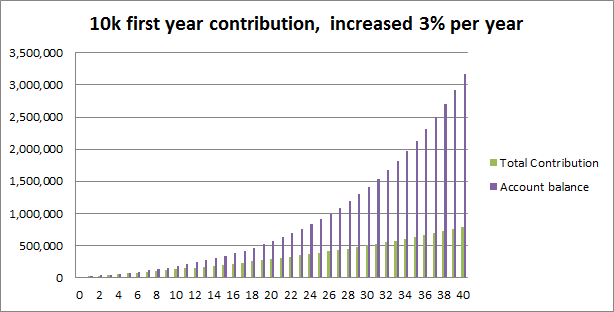

In my previous post, I hinted at why putting your money away in a checking account may not be a good way to save for retirement. Let’s compare this strategy with investing the money saved away. Consider this graph which I used for another post (“The power of compound interest”) a while ago:

After 40 years, by investing your money, you will end up with 4 times the amount you contributed. 4 times. In other words, investing your retirement saving basically cuts the amount you need to save by 75%. Instead of saving 40k per year, now you only need to put away 10k per year.

Continue reading The basics of retirement savings: why “saving” may not be enough

The basics of retirement savings: why you need to start now

OK, let’s face this. I am in my 20’s. If you are reading my blog, you are probably in your mid-20’s as well. What’s up, retirement? Geez, why care about anything 40 years out?

Well, I’m an actuary, so I speak in terms of probability. What if I’m one of the (un)lucky few bastards that make it past 65 years old? Well, first off, I will most likely be out of jobs. And secondly, my health will not be cheap. Think more doctor visits, more ways to exercise, healthier food, higher health insurance premiums. And I may want to give something to my grandchildren if they choose to attend Harvard….

Where does the money come from?

Continue reading The basics of retirement savings: why you need to start now

AAMRQ-AAL final conversion formula and equity distribution plan explained

As you know, this summer I wrote two blog posts on the AMR Corporation and US Airways Group merger to explain how it affects AAMRQ stock price. Using the information available at that time I derived a formula to estimate AAMRQ stock price based on LCC stock price:

I know I mentioned that I would write more about the AAMRQ stock case if there was a huge surprise. And there was a huge surprise when the Department of Justice filed an antitrust lawsuit against AMR Corporation and US Airways Group, but this happened when I was entangled with a few life issues, so I had to skip.

Not to say that I am much less busy now, but I thought this case deserves another mention. Caution: math abound 😉

Continue reading AAMRQ-AAL final conversion formula and equity distribution plan explained

Hiep’s Finance ‘s final formula for AAMRQ-LCC conversion

I don’t have much time to comment much on this merger right now, so I will just go ahead and post what I consider to be the final AAMRQ conversion formula:

AAMRQ stakeholders officially receive 544.4 million AAL shares. Each AAL share is worth an LCC share. Using the approximate number of AAMRQ shares outstanding 335.5 million, and the approximate debt of $8 billion, the share conversion formula is:

Continue reading Hiep’s Finance ‘s final formula for AAMRQ-LCC conversion