After achieving a 760 FICO credit score, I thought the next milestone would be 800. Since there are multiple FICO scoring models that lenders use, an 800 FICO would almost guarantee me at least a 760 on other FICO models. My credit history length is hitting 3 years in January 2015, and my AAoA (average age of accounts) is going to reach 2 years in February 2015. Since FICO scores tend to increase at these factors’ milestones, my score is probably going to achieve the maximum in February 2015 before hitting the plateau. And since I have several credit inquiries from the auto loan applications in February 2014, in February 2015 when they drop off, I’ll have a decent shot at an 800 FICO.

Today’s feature: Discover It credit card review

2 years ago, when I had just started this blog, the Discover More was one of the first credit cards that I reviewed. Since then, Discover Financial Services has replaced the card with the Discover It which is in many ways the same as the Discover More. I personally still have the Discover More, but most people these days have already switched over to the Discover It. It is about time I reviewed the Discover It as well.

Continue reading Today’s feature: Discover It credit card review

Why paying off your loan is bad for your credit

Recently, a friend of mine asked me if he should pay off his auto loan he had acquired years ago. While the interest rate on the loan is very low, less than 3%, he wanted to be free of debt and felt tempted to finish making monthly payments for the loan. He makes good income and is very disciplined about expenses, so paying the remaining balance would not cause any financial burden to him, and neither would maintain the monthly payments. His main concern was the impact on his credit.

I talked him out of it.

Continue reading Why paying off your loan is bad for your credit

How I achieved 760 FICO credit score in just over 2 years

How I achieved 760 FICO credit score in just over 2 years

My credit journey has now lasted for 2 years and 10 months, and I’m in the mood for reflecting on the journey thus far. I did a lot of research about credit along the way, especially in the first year, to make sure I could achieve the most, credit-wise, in the shortest amount of time. And at this moment, I am about exactly where I wanted to be, and in just about the best position there could be for someone with 2 years and 10 months of credit history.

760 FICO credit score has long been considered a hallmark of excellent credit, and I hit it about 3 months ago.

Continue reading How I achieved 760 FICO credit score in just over 2 years

Step-by-step guide to build credit in one year

I have written this guide as a balanced approach to building credit if you are starting out. It is not intended to give you the maximum credit score, since that would require that you know perfectly how to manage credit from the beginning, an unrealistic expectation. If you follow this guide, at the end of the first year you should have a solid credit history that would allow you to get approved for most credit cards and obtain reasonable interest rates on auto loans.

Continue reading Step-by-step guide to build credit in one year

How do I improve my FICO credit score in a month?

Even though I said that a good FICO credit score takes a long time to build, there are situations where time is against you and the last few points really matter. Many mortgage lenders have FICO score thresholds for interest rates, and you may fall a few points short of the next threshold which may mean thousands of dollars’ worth of payments. You don’t have another few years to carry your FICO score to that threshold. So what to do?

Continue reading How do I improve my FICO credit score in a month?

Why are FICO credit scores important?

Your credit score is a number that represents your creditworthiness. It is a number calculated from your credit history based on an algorithm to predict how likely it is that you will default on your debt. While your credit score is not the only thing that determines the outcome of your mortgage or auto loan application, it is one of the most crucial factors, if not the most crucial.

Today’s feature: MyFICO Score Watch product review

I wrote in “Personal Finance 201: Credit scores” about how FICO scores are almost the only credit scores that matter. Most large financial institutions such as Bank of America, American Express, Discover Financial Services, and Citigroup, rely on FICO scores for creditworthiness measurement. Knowing your FICO scores is helpful in timing your credit application; a few points difference in credit scores can translate to thousands of dollars of payment on your mortgage.

Based on the table above, the difference between the first category and second category of credit scores translates to a difference between a 4.236% and a 4.014% on 30-year mortgage loan. For a $300k mortgage loan, the difference in payments is approximately $39 per month, which comes out to be around $460 per annum, or $14,000 over the duration of 30 years.

Continue reading Today’s feature: MyFICO Score Watch product review

The ideal number of credit cards: why/when more is better

When I started my credit journey in January 2012, all I wanted at the time was the first card, and I stayed with one card for the next 9 months until I learned that there were better cards in the market. For the next 3 months I went on an app spree and finally came to the point where I felt adding another card to my portfolio wouldn’t do me much good any more.

Apparently the number of credit cards I have is absurdly high to many people. The common perception is that more credit cards suggest more financial trouble. Knowing that a high percentage of the population tend to abuse credit and get themselves into a debt spiral, I totally understand how this perception was created.

Needless to say, if you have had credit before and found yourself often charging credit cards up to the maximum allowed and not paying the balance in full, 1 credit card is enough. You still need a credit card to maintain your credit history, but for that purpose one card can be sufficient if you do not abuse it. On the other hand, if you are able to handle credit well, never charge to the limit, and always pay statement balances in full, then you should have multiple credit cards. If you want to know the reason, please read on.

Continue reading The ideal number of credit cards: why/when more is better

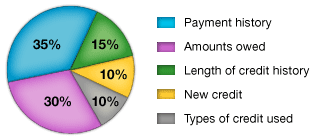

The must-know graph for credit scores

The chart from FICO, the company that provides the most widely used credit scores, says it all:

That is it, folks. To achieve a high FICO credit score, we only need to improve these 5 components. In order of importance, here are the 5 things we should do to increase our FICO scores: